If you put your new home search on hold this year, this could be the right time to reignite that mojo engine!

We often hear of buyers putting their search on hold for various reasons. This last couple of years, the reason has typically been the economy. We can’t deny that affordability in this economy has been a challenge. In 2020, with mortgage interest rates in the 3% range, the NATIONAL ASSOCIATION OF REALTORS Quarterly Housing Affordability Index1 reports a Composite Affordability of about 170. Compare this to the more recent 3rd Quarter 2023 (projected)at only 93.4. (see https://cdn.nar.realtor/sites/default/files/documents/hai-q3-2023-quarterly-housing-affordability-2023-11-09.pdf?_gl=1*wd9xk6*_gcl_au*MTQwMDA3OTY4LjE2OTgyNTM2Mjk.)

However, this information lags as it takes time to compile the national statistics. Rates have started to come down and economists are seeing light at the end of this tunnel helping to make housing more affordable.

When will rates come back down?

No one really knows the exact answer to this question. Economists are beginning to expect the Federal Reserve to start cutting rates toward the end of the 1st quarter of 2024. We’ve already seen improvement during November 2023. And this week’s jobs report supports holding rates steady at next week’s Federal Reserve meeting. Note that no one is teasing previous 3% mortgage interest rates as we saw before the sharp run up. What many do expect is to see rates between 5-6%, and when that happens, many buyers will jump back into the market causing a surge in demand. This increase of buyers will cause the real estate market to catch fire once again. We suggest that the trick is to re-enter the market before it over heats. Since there may be some good deals in the next couple of months, consider the benefits in actually buying now, at the end of the year and into early 2024.

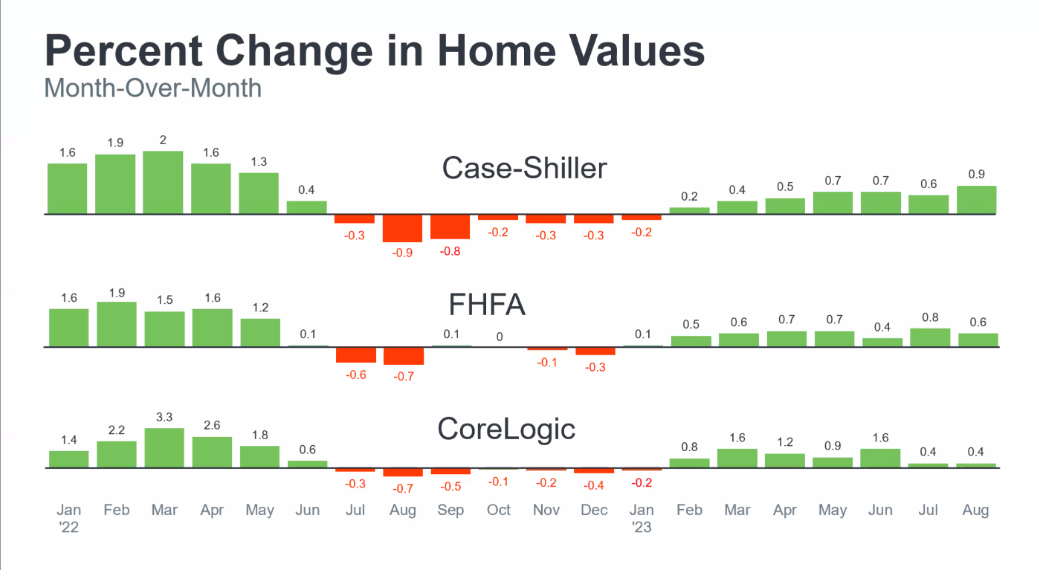

But, if you buy now will home values begin or continue to drop?

Many people are under the impression that home values are going down. While this may have been true in some segments in 2022, prices have actually increased in 2023 due to the shortage of housing inventory. The price increases have not been at the same fast pace as in 2020-2022 but, prices in many markets have increased this year. See chart above, “Percent Change in Home Values” that shows 3 different home value trackers, Case-Shiller, FHFA, and Core Logic. Sometimes, however, there are good prices discounts as we slide into year end. Herein lies your opportunity; buy before prices begin to rise again in 2024 as the market heats up again.

Is there a recession around the corner?

A recession could decrease home prices, and that can be worrisome. However, the number of economists that had predicted a recession brewing back in 2022 has now decreased with many indicating that the “soft landing” was achieved instead. See Wall Street Journal, Harriet Torry and Anthony DeBarros on 10/15/23, “A Recession Is No Longer the Consensus,” https://www.wsj.com/economy/a-recession-is-no-longer-the-consensus-3ad0c3a3.

Additionally, a big reason that housing prices drop during a recession is because of the increased fear of job loss. However, recent data shows that the labor market remains strong. The November 2023 unemployment rate trended down to 3.7% which is well below the 75-year average of 5.75%. There is always the possibility that the unemployment rate may start to increase, but there is a lot of room before we hit this average. See Wall Street Journal, Amara Omeokwe and Nick Timiraos on 12/8/23, “Economy’s Soft Landing Comes Into View as Job Growth Slowly Descends,” https://www.wsj.com/economy/jobs/jobs-report-november-2023-us-economy-59125cde?mod=djemalertNEWS . And, we are not experiencing any meaningful uptick in housing foreclosures; another metric of recession. Foreclosures remain low mostly due to low interest rates and increased home values (read equity). Further, mortgage delinquencies are at their lowest ever which does not suggest any early stage foreclosure activity.

Notwithstanding the metrics pointing away from a recession, if one did hit, it does not necessarily follow that housing prices will drop. It was definitely true in 2008 during the Great Recession because housing actually led that recession. And, it was true, to a much smaller extent, in 1991. Today, most homeowners are sitting on a lot of equity and low rates. This means that supply will remain low and many buyers will compete for fewer homes. This does not suggest price drops!

At the end of the day, life situations and goals typically drive timing for families wanting to buy a new home. In general, if you can afford to buy that new home now, there is a good window of opportunity to lock in a good price now and then watch your equity grow in 2024. We don’t expect this lull to last much longer. Contact Team Plunkett to explore your options!

________________________________________

Footnotes:

- The Housing Affordability Index measures whether or not a typical family earns enough income to qualify for a mortgage loan on a typical home at the national and regional levels based on the most recent price and income data.