High mortgage rates, particularly coupled with an unstable lending environment, lead to challenges for both buyers and sellers. Various creative financing options can help make homeownership more accessible and affordable thus solving some of these challenges.

In a typical conventional financing scenario, a buyer makes a 20% down-payment in order to purchase their new home while financing the remaining 80%. The buyer, or borrower, makes principal and interest payments on a fully amortizing mortgage over 30 years. For those that have more wealth to lean into (either their own or through a family gift), other attractive options can be “all cash” deals, 15-year mortgages, or maybe even lease-to-buy arrangements.

Buyers may benefit from other financing options for affordability or flexibility reasons:

-

Interest-Only Mortgages – Interest-only mortgages offer borrowers the flexibility of making payments of only interest for a specified period, typically the first 5, 7, or 10 years of the loan term. This results in lower monthly payments initially, providing breathing room in a high-rate environment. Not only is the monthly mortgage payment lower due to no pay down of principal in that initial period but the interest rate for these loans is often a bit lower than fixed interest mortgages. However, after the interest-only period ends, the loan converts to a traditional principal and interest payment structure amortized over the shorter remaining period of 25, 23, or 20 years resulting in a large increase in the monthly mortgage payments, especially if the prevailing rates have increased. Interest-only mortgages are suitable for buyers who either anticipate an increase in income or plan to sell or refinance the property before the interest-only period expires.

-

Seller Buy Downs – Seller buy down programs require a payment by the seller at close of escrow that essentially pre-pays a portion of the buyer’s mortgage interest thereby reducing the buyer’s initial monthly payments. It is much like the buyer paying “points” on their loan but, in this case, the seller makes this payment to the lender as a “seller concession” to the buyer. This can make the home more affordable and attractive to buyers, particularly in a market where interest rates are climbing. The pay down can cover the first year, two years, or maybe even three years. At the end of that period, the buyer will likely benefit by selling or refinancing the property when rates are lower. Seller buy downs can be negotiated as part of the home purchase agreement and are beneficial for both buyers and sellers looking to close the deal. If there are multiple offers on a home, the buyer may need to sweeten their offer to be competitive with the other buyers that are not asking for this seller concession.

-

Departing Residence Programs – Departing residence programs, also known as bridge loans or swing loans, provide short-term financing to homeowners who are purchasing a new home before selling their current one. These programs allow buyers to obtain new mortgages to purchase their new home without the expenses of their existing homes counting against them in the lender’s qualifying calculation because the buyer is promising to sell their existing home, or rent it out, soon after making their purchase of a new home. Departing residence programs are ideal for homeowners who want the convenience of finding their new home before selling their current home. It also makes their offer on their new home stronger than if they were making a contingent offer (an offer where the purchase is contingent on the sale of their existing home). In order to qualify for this program, the buyer needs to have other funds for their downpayment and closing costs of the new home and they must have good equity in their current home.

-

VA Loans – VA loans, guaranteed by the Department of Veterans Affairs, offer eligible veterans, active-duty service members, and their spouses competitive financing options with no down payment or private mortgage insurance (PMI) required. VA loans are particularly valuable in a high-rate environment, as they often offer lower interest rates compared to conventional loans. Additionally, VA loans have flexible qualification criteria, making them accessible to a wide range of borrowers. Team Plunkett has successfully closed several VA loan deals that all went very smoothly. These are fantastic tools for those that qualify.

-

Doctor and CPA Loans – Doctor loans, also known as physician loans, cater to medical professionals, including doctors, dentists, and veterinarians, who may have high earning potential but limited down payment savings. There are similar programs for CPAs. These specialized mortgage products typically offer higher loan amounts with reduced down payment requirements and lenient underwriting guidelines. Lenders count on the upward trajectory of the professional’s income in the future. Doctor loans are a great option for medical professionals looking to purchase a home in a high-rate environment without depleting their savings.

-

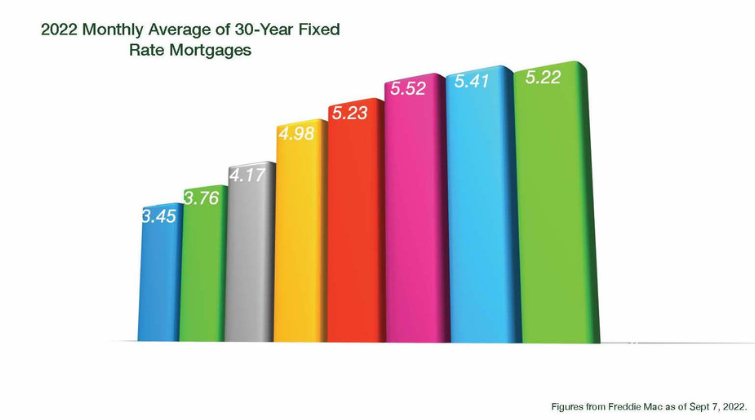

Assumable Loans – Assumable lower-rate loans are a rare and hidden prize in the mortgage world. Here, the buyer steps into the shoes of the seller and becomes liable on the seller’s current mortgage. The lender would have the ability to qualify the buyer in order to protect their interests. In California, 85% of current homeowners have mortgages with rates at or below 5%. That makes a big difference as compared to current rates hovering near 7%. On a $1,000,000 loan, the lower monthly payment at 5 % would save the buyer $1,285 per month (from $6,653 to $5,368). The unfortunate reality here is that most sellers do not have assumable loans to pass on to buyers..

-

Seller Financing – Another occasional situation to take advantage of, if you are lucky enough to come across a seller that does not need his cash out from the sale right away. Seller financing puts the seller in the position of seller and lender. A promissory note is executed and the buyer makes mortgage payments directly to the seller, typically in monthly installments, until the loan is fully repaid. Seller financing can be advantageous for both parties, as it allows buyers to bypass traditional lenders and potentially negotiate more favorable terms, such as a lower down payment or interest rate. Additionally, seller financing can facilitate transactions in a high-rate environment by offering an alternative financing option when conventional loans are less accessible or less affordable. Sellers who own their properties outright or have substantial equity may find seller financing an attractive way to attract buyers and close deals quickly.

Team Plunkett often works with these different financing products and can help you determine if one of these scenarios can benefit you. More importantly, we can connect you to solid lenders that offer these programs. The goal in this high interest environment is to get you into the home that you want before the rates drop and the subsequent competition amongst home buyers heats up. The biggest expense to a buyer is the equity bump that they might forego by delaying their home purchase.

Contact Team Plunkett today and put our knowledge to work for you!