Are you putting your home search on hold until the interest rates come down? As with all things, there is a cost to this strategy and understanding that cost may change your perspective.

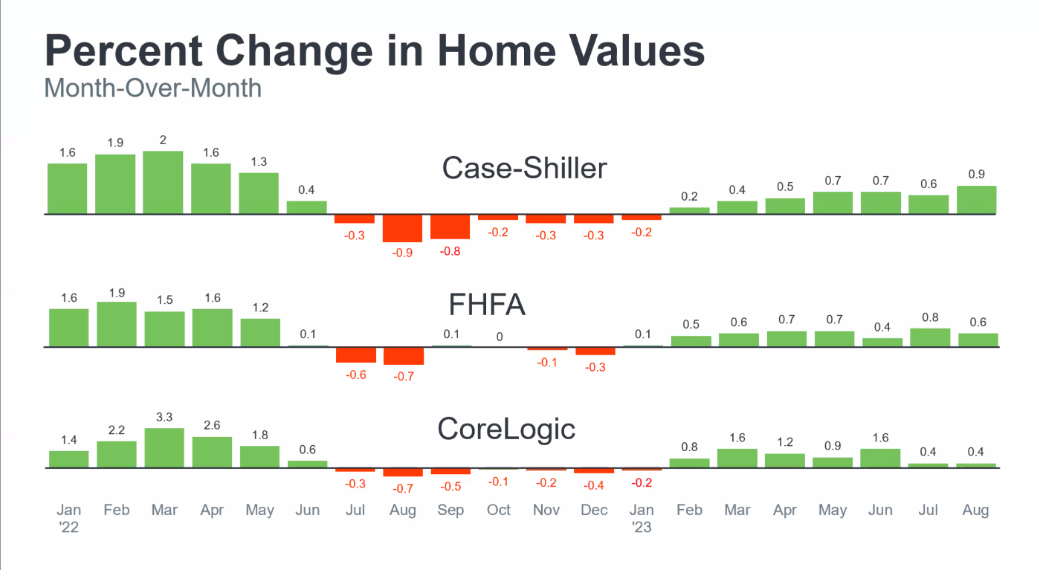

When mortgage interest rates began climbing at a dramatic pace in May of 2022, many expected home values to drop too. However, due to the very low number of homes available for sale, this did not happen. In fact, home values continued to grow but at a slower speed. Home values are expected to continue to rise as inventory remains scarce. While your home purchase is on hold, life continues to move forward and homes continue to appreciate. It is obvious to us that higher mortgage interest rates are a direct cost to buy a home but it is easy to forget that there is also a cost to delay a purchase while waiting for a drop in mortgage rates. However, the cost of leaving home appreciation on the table while you wait creates bigger impact on your wealth than the current cost of the mortgage interest rates. Especially if your purchase will be for the long term where appreciation will keep growing.

Lawrence Yun, Chief Economist at the National Association of Realtors, has predicted home values will increase 15-25% in the next 5 years. But, even if home values drop at some point in the near future, such a drop would be very short term since housing inventory is so scarce and is expected to remain so. The low supply will naturally quickly drive values back up. Over the long term, home appreciation is a solid bet.

While we expect rates to drop, we will likely not see the 3-4% mortgage rates again soon, if ever. So, how long do you want to wait for a 5-6% loan versus a 6-7% loan. The longer you wait, the more home appreciation you are passing on. Savvy buyers can take the 6-7% loan now and bank their appreciation knowing that when the time is right, they can refinance their loan in the future into a lower rate mortgage.

For example, while waiting for mortgage rates to fall to 5% you forgo a 6.75% rate today on the purchase of a $1,000,000 home, saving you $14,007 of “excess mortgage interest” ($53,739 interest at 6.75% versus $39,732 interest at 5%; ). However, you have left $50,000 of home appreciation on the table. Net cost to you is $35,993.**

Thinking about waiting another year? Lost home appreciation is now $102,500 while “excess mortgage interest” savings for 2 years is $28,014. Net cost is $74,486. Waiting a third year can cost you $157,625 in home appreciation while saving you a cumulative $42,022. This net cost to you is $115,603.

It is also important to note that when the mortgage rates do start coming down, buyer demand will increase as everyone on the fence now starts to jump back into the market, causing another heated market where buyers will be forced to fiercely compete against many other buyers to get their new home. Why not beat everyone to the finish line?

Contact our team to put a plan in place for your purchase.

** Assumptions: 1) 80% LTV on a 30-year loan and 2) 5% increase in home values each year.